The latest Energy Information Administration (EIA) Annual Energy Outlook has been released and one’s hope, on first glance, is that this forecast is just as off as so much of energy forecasting has been because, if this is accurate, the simplest summary of this might be:

The United States and humanity is EFFed when it comes to an opportunity to mitigate climate change through reduced energy emissions.

The critiques of EIA forecasting abound (see short bibliography here). Adam Scott well captured the situation last September in discussing the just-released International Energy Outlook (IEO).

Should EIA forecasts come with a warning label? (Courtesy: Price of Oil)

the EIA has made a routine out of releasing unrealistic, distorted, and dangerous outlooks on the future of global energy demand. These projections should come with a warning label.

Now, a forecast is that — an effort, with a set of assumptions, to delineate what the future might portend. Recognizing that forecasting is, well, hard and that there will always be errors, the question is how to leverage forecasting work. What is truly useful, in such endeavors, is to have multiple looks (scenarios) with seeking to understand what commonalities exist across scenarios, what assumptions drive change, and key uncertainties. Understanding those, rather than having a projection of oil production to three decimal points a decade from now, helps planning and investment across society. Leveraging a specific scenario forecast (typically the ‘baseline’) as core to investment decision-making creates (significant) risk (see GE troubles as evidence case #1) and failures to have an appropriate range of scenarios to span plausible futures also creates significant risk.

On first review of the WEO’s 54 page summary, striking elements include:

- In contrast to what has occurred over the past decade,

- after a decade of decline, carbon emissions are projected to increase steadily through 2050;

- reversing significant decline, coal use is projected to rebound somewhat and remain stable through 2050.

- carbon intensity (how much pollution per dollar of economic output) improvements slow.

- as do essentially all trend lines favorable to a clean energy future.

- Seemingly ‘between the lines’ efforts to satisfy/engage Trump Administration bias and priorities

- While “carbon” and “carbon dioxide” are in the report along with discussions related to the Clean Power plan, “climate change” and “global warming” are terms absent from the report. (Why does “carbon” matter if …?)

- Coal’s future is more constrained because of “as a result of supportive policies for renewables compared with coal” [page 16] rather than a more honest reality that coal, increasingly, simply can’t compete with clean electricity options (solar and wind, primarily) and natural gas.

- Note that the same bullet asserts that there “favorable market conditions for natural gas” and nothing is evident along these lines in relation to how wind/solar prices are plummeting and thus there are “favorable market conditions” for these electricity options.

- A bizarrely aggressive forecast as to nuclear power pricing, suggesting roughly a 50 percent drop in “advanced nuclear” project pricing in the coming five years. (See graphic below.)

- A very rosy projection for shale (both fossil gas and oil) that might be far from viable.

- Renewable energy price forecasts are unreasonably high.

- Forecasted prices for 2022 for both wind and solar are well above what are already being bid into commercial contracts.

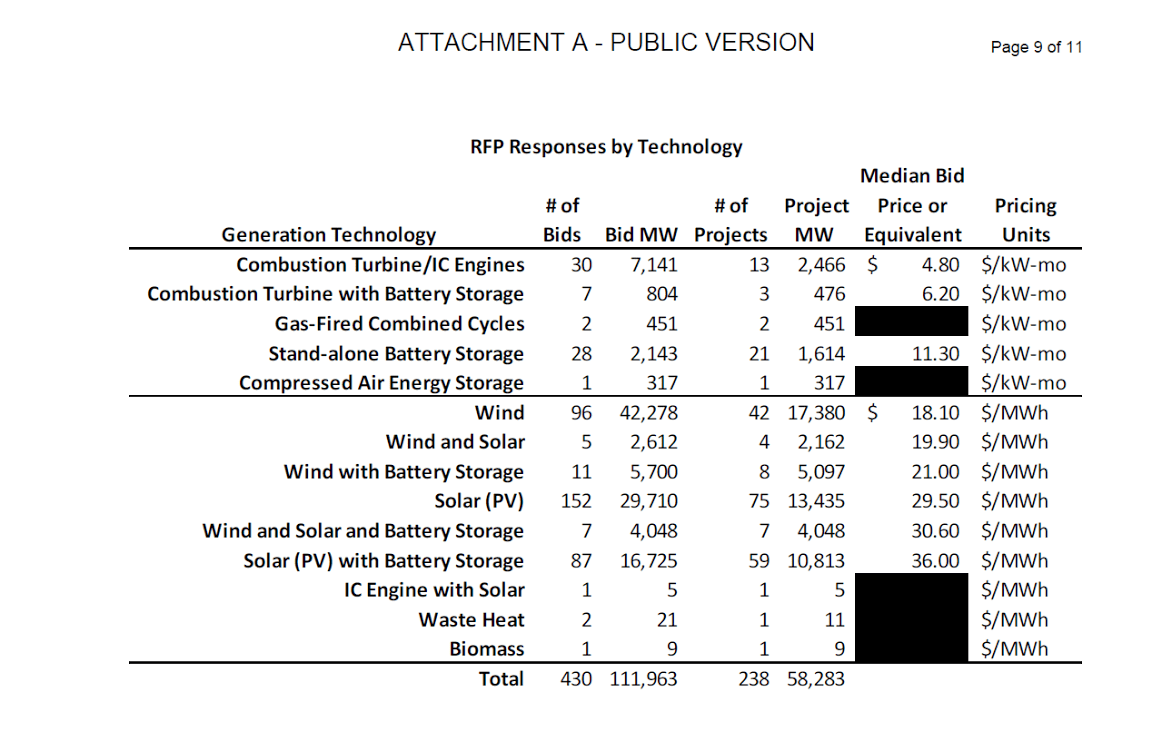

- The levelized cost of electricity (LCOE) is projected (see graphic below) to be in the ballpark of $30-$60 per mWh for new wind projects. Xcel Energy, in Colorado bids, had median prices of under $20 for wind and with with battery storage was just $21.

- Solar LCOE is projected slightly above wind, in the $35-$70 range. Going back to Xcel, the median price for a 2023 solar project was $29.50.

- Forecasted prices for 2022 for both wind and solar are well above what are already being bid into commercial contracts.

{kind=link}

EIA forecasted 2022 electricity project pricing (Annual Energy Outlook, 2018, page 16 https://www.eia.gov/outlooks/aeo/pdf/AEO2018_FINAL_PDF.pdf)

- Failure to include a realistic ‘aggressive’ clean energy futures alternative scenario

- Globally, renewable energy (primarily wind and solar), storage, and associated systems (smart grid/power management/energy efficiency/electric vehicles) are booming with rapidly growing market shares, new innovations (technical, financial, business processes) emerging every day, and prices plummeting faster than almost any specialist expected to happen even just a few years ago.

- As to the last, solar and wind project bids are increasingly coming in at lower prices than what is being paid for existing coal (and nuclear) electricity production.

- IRENA forecasts that by 2020 renewable energy will be cost-competitive (if not cost advantaged) against fossil fuel (including natural gas) electricity production in most of the world.

- Electric vehicle (batteries and otherwise) prices are falling fast and the ‘cost to own’ an EV, in much of the world, already below that for a traditional gas engine with projections along the lines of “within 20 years, if trends hold, 200-mile-range 4-seater EVs, with awesome acceleration and modern amenities, will be cheaper than the cheapest cars sold in the US today.”

- While the baseline is absurd in the low-ball projections of these to 2050, what is even more concerning is that the EIA WEO does not have an “aggressive clean energy penetration” alternative scenario that comes anywhere close to projecting a possible (actually plausible) path forward for renewable energy.

- For example, consider that point about electric vehicles: if in 2040, EVs are ‘cheaper than the cheapest cars sold in the US today”, why would (as per the EIA forecast) EVs hold less than 20 of the total market in 2050? An aggressive scenario might more appropriately postulate long-range EVs at 75 percent market share by 2050.

- Globally, renewable energy (primarily wind and solar), storage, and associated systems (smart grid/power management/energy efficiency/electric vehicles) are booming with rapidly growing market shares, new innovations (technical, financial, business processes) emerging every day, and prices plummeting faster than almost any specialist expected to happen even just a few years ago.

Examining what is happening in the real world, that absent ‘aggressive’ clean energy scenario might be the most realistic one while also being one where US energy carbon emissions fall and the nation is on the path to serious climate change mitigation.

Like an observer impacting the observed, forecasting impacts the real world through helping inform and drive investments. Strong forecasting enables decision-makers a window as to their options and enables more informed decision-making even in the face of the uncertainty that is the future. Flawed forecasting undermines sound decision-making and can create significant harm into the future. The EIA forecast suggests that renewables are marginally competitive with, for example, new nuclear power plant projects. This, quite simply, has no basis in the real world. Making investments with a belief that EIA forecasting is sound creates risk for ill-advised investments and an increased likelihood of the financial havoc of even more stranded fossil-fuel assets in the decades to come.

Sigh … going back to Adam Scott

For anyone who actually wants to use energy forecasts as a tool to inform sound decision-making, for directing investment wisely, and for meeting the obvious goal of achieving climate safety – we need outlooks with credible assumptions. It’s a shame we can’t trust the EIA to provide them.

NOTE: Sadly, to make clear, this is a recurrent problem with EIA which has consistently been underforecasting renewable energy system penetration. ;asldjkf See, for example, Department of Energy’s “Annual Outlook 2015” is out: what do we know w/out reading it? For a selected bibliography on this, see end of When it comes to renewable energy forecasting, Japan’s forecasting follows world lead.

UPDATE: Some material post posting of relevance:

- Dan Cohan, New projections play up coal while downplaying renewables — that’s not reality, The Hill. Excellent review of problems in AEO2018, with focus on issues raised above with supporting details/analysis.

- John Cushman, No Drop in U.S. Carbon Footprint Expected Through 2050, Energy Department Says, Inside Climate News

- Several twitter threads of relevance:

1. No scenario analysis around the cost of solar, wind and battery storage. Costs have declined rapidly, and are expected to continue to. EIA uses scenarios to show oil and gas technology cases. Why not the same for technologies with more technology cost uncertainty?

— Brendan Pierpont (@brendanpierpont) February 6, 2018

1. As usual, bad news for climate. EIA projects CO2 to stay flat, with electric sector surprisingly retaking the lead from transportation (due to car & truck fuel economy standards through mid-2020s). Oil & gas continue to be top sources of emissions. #AEO2018 pic.twitter.com/9Xqb2Jxh9h

— Daniel Cohan (@cohan_ds) February 6, 2018

EIA still vastly overestimates the cost of utility-scale solar:

$2.00/Wac (tracking) and $1.76 (fixed) in 2019.https://t.co/NPGrF3qG3zNREL reports costs were actually $1.11/Wdc (tracking) and $1.03 (fixed) in 2017.https://t.co/cG2CeS1ujM

— Daniel Cohan (@cohan_ds) February 8, 2018

1 response so far ↓

1 The Gigafactory’s new neighbor: Gigawatt // Feb 8, 2018 at 9:11 pm

[…] ← New EIA forecast subtitled: We are EFFed … […]